Mortgage Shopping: What Buyers Should Know About Loan Estimates

For most buyers, shopping for a home is a lot more enjoyable than shopping for a mortgage.

While mortgage shopping may never be “fun,” the Consumer Financial Protection Bureau (CFPB) wants to help eliminate some of the past frustrations consumers have experienced. The CFPB was created in 2010, with the passage of the Dodd-Frank Wall Street Reform and Consumer Protection Act.

In 2012, the CFPB took steps to “simplify and improve mortgage disclosure forms” and make it easier for consumers to find the best loan value, and to compare “apples to apples” in loan products. The Bureau also cut the number of disclosure documents to two: a Loan Estimate form and a Closing Disclosure form.

The resulting “Know Before You Owe” mortgage disclosure rule went into effect on October 3, 2015.

Disclosures Simplified

The new forms are easier for borrowers to read and understand than their predecessors, which contained overlapping information and “inconsistent language,” according to the Bureau.

Simple language and detailed instructions (on how to fill out the forms) helps to guarantee the consistency of information that lenders provide to borrowers.

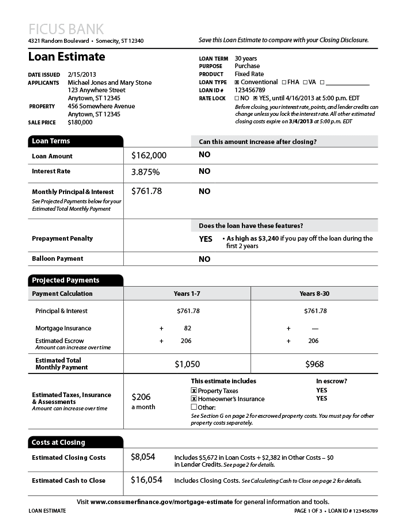

The Loan Estimate Form

This new Loan Estimate form replaces two old forms (the Good Faith Estimate from the Department of Housing and Urban Development and the early Truth in Lending disclosure from the Board of Governors of the Federal Reserve System), as well as including new disclosure information required by the passage of the Dodd-Frank Act.

The Loan Estimate is a standardized form that lenders must give borrowers within three business days of submitting a loan application. The goal of the three-page form is to provide information on a loan’s:

- Key features

- Costs

- Risks

Borrowers can apply for loans from several lenders and compare their Loan Estimate forms side by side, making a more informed decision on which loan product is best for them.

The requirement for lenders to use these forms applies to most home mortgages, with a few exceptions:

- Low volume creditors (those making five or fewer mortgages in a year)

- Home equity lines of credit

- Reverse mortgages

- Mortgages on a mobile home or dwelling not attached to land

The Loan Estimate form outlines important details for buyers, including:

- The loan amount

- Monthly mortgage payments

- The length of the repayment

- Interest rate (and how long it’s locked in)

- How much is being held in escrow and for what purpose

- Estimated closing costs and cash needed to complete the closing

- Fees for services (broken down by those you can shop for, and those you can’t)

- If the loan is assumable

Additionally, a box on the third page of the Loan Estimate form gives information on how much principal will be paid off in five years, and how much of the interest, mortgage insurance, and other loan costs will have been paid during that same time.

This, along with additional details in this section, makes it easier to compare loans and for the borrower/buyer to select the best loan product for their needs.

The CFPB’s site comprehensively explains a sample Loan Estimate form, walking borrowers through the details you should check, as well as definitions for items on the form.

Watch for part two of this article, which explains the second new form, the Closing Disclosure. This form is longer, but “mirrors” the information on the Loan Estimate, making it easy for borrowers to compare the promised terms and conditions, to final mortgage costs and details at closing.